Rising M&A deal diversity

Strong M&A activity slated to continue

Through most of 2023, the market for mergers and acquisitions has been challenging, but the life sciences industry has proven to be resilient and active, particularly for corporate strategic acquisitions, along with a near record-setting pace of divestitures. We anticipate 2024 will continue the trendline to resemble 2019-2020 in terms of deal value and volume. Divestitures and restructurings will also remain prevalent, although likely not at the values seen in 2023. We also expect to see increased joint venture creation as a way to extract value out of non-core assets.

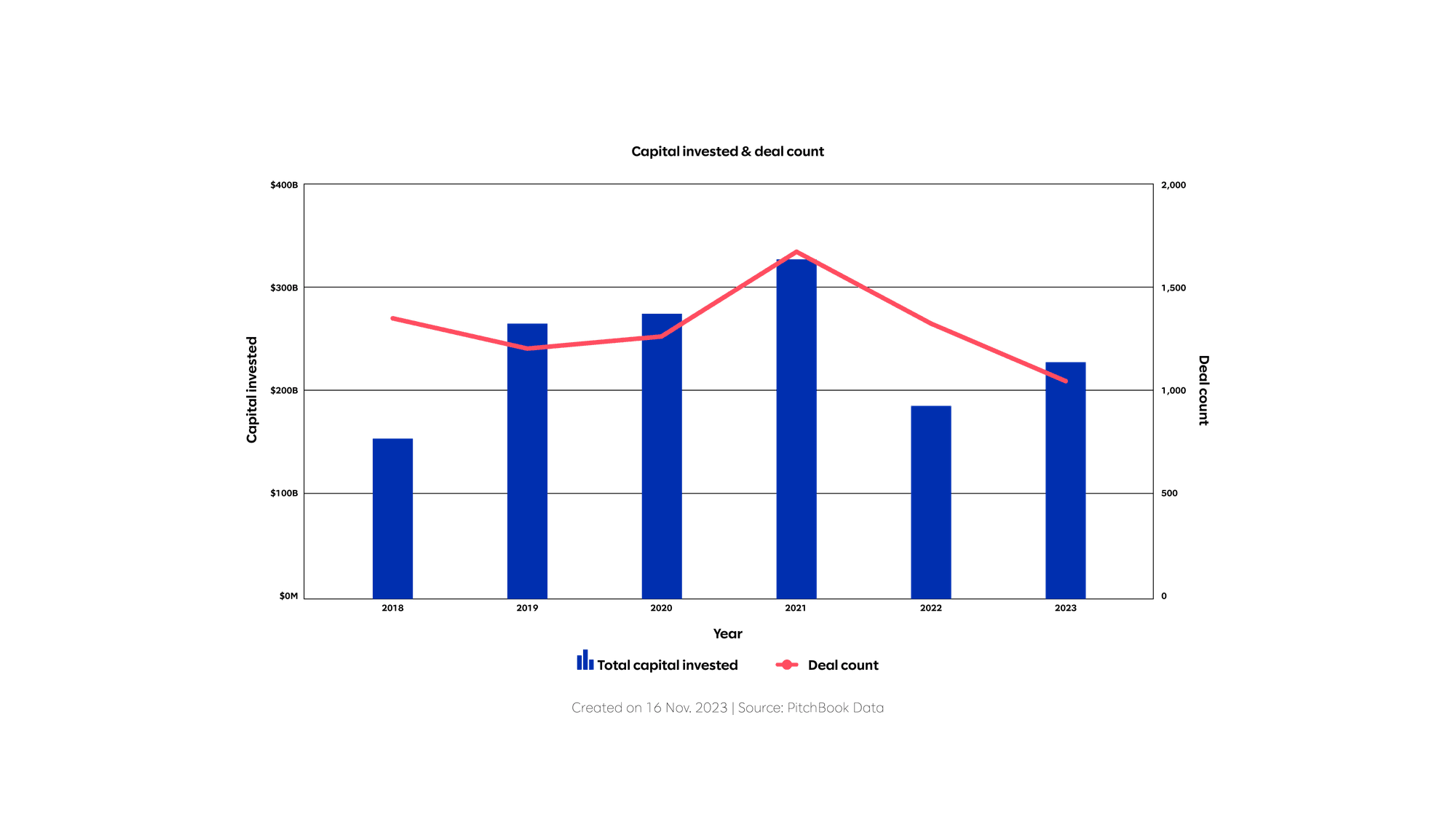

According to Pitchbook data, the total overall deal value in life sciences acquisitions increased in 2023 compared to 2022, even though the volume of deals was lower—this was due to a handful of significant megadeals in the industry. We expect this trend to extend into the early part of 2024, with a number of significant serial acquirers indicating a desire to expand dealmaking and the corresponding balance sheets to support that activity.

Life sciences M&A control transactions 2018-2023

Navigating risks with cautious deal structures and clear ROI

The current challenging economic climate and deal financing conditions have forced companies to be less willing to take risks in creating value. This is impacting the types of deal structures being built and how executive and corporate development teams are planning and executing integration.

Earnout and milestone-based deal structures have long been favorites of large-cap life sciences companies buying biotech and clinical-stage targets. We expect acquirers to be even more aggressive in implementing these structures to mitigate downside risks further, given the tight financing and economic environment. However, it’s important for targets to be aware of what they are agreeing to and account for the heightened possibility that those milestones may never be achieved. Fierce Biotech indicated in a recent article that achievement rates of key acquisition milestones have decreased across the industry.

Integration planning has become heavily scrutinized to ensure synergies are delivered as expected. Companies are now placing greater emphasis on cost synergies that can be easily evaluated instead of revenue synergies that are harder to audit. CFOs will expect integration teams to deliver unassailable deal value as they face a tougher task in building and defending underwriting cases under more conservative and demanding financing scrutiny. Integration teams should anticipate those expectations and, in turn, be thorough in building and documenting synergy initiatives.

Increased joint venture activity and diversity in deals

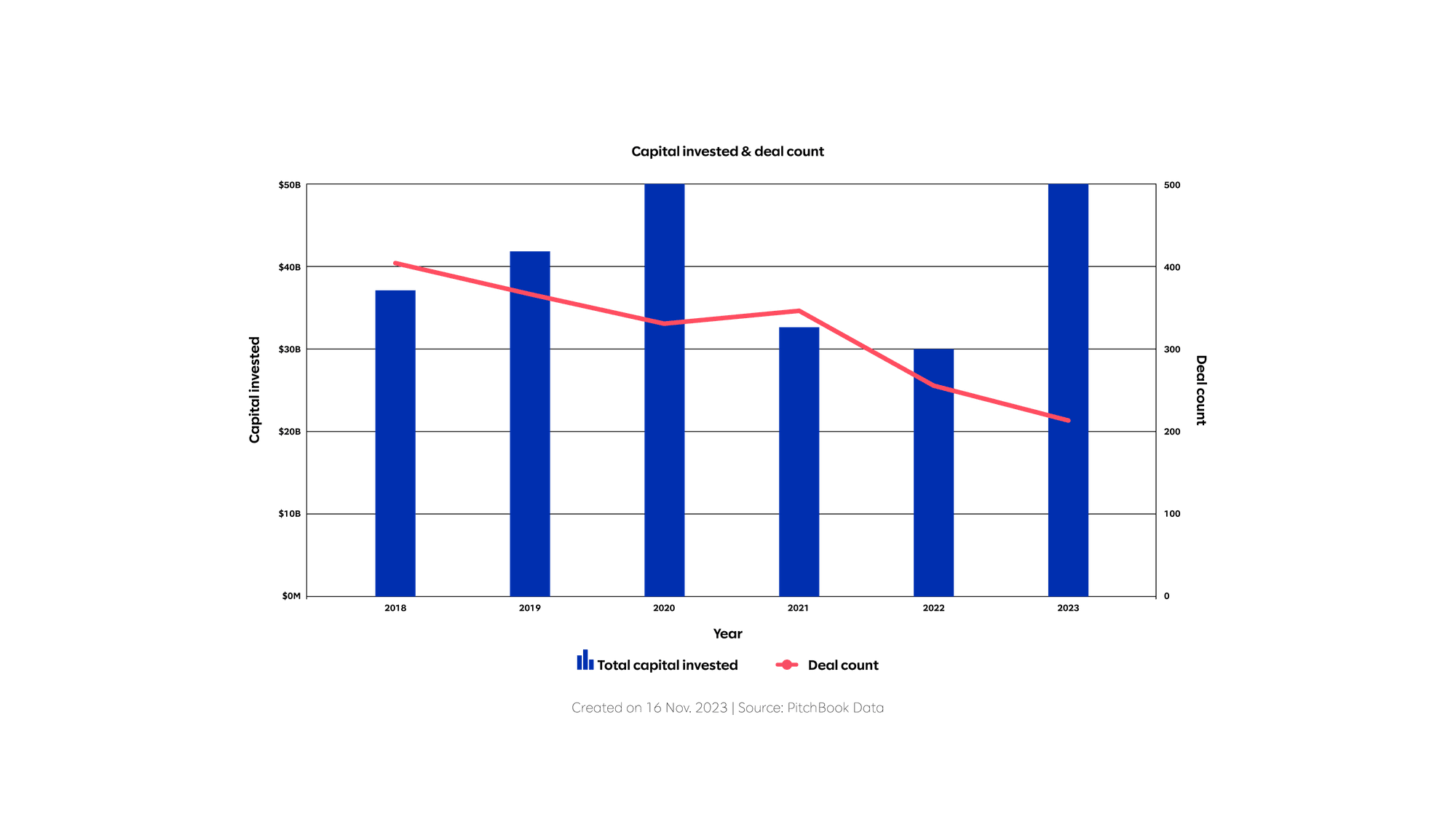

There is an ongoing popularity of divesting non-core assets, and we expect additional joint venture activity to increase in 2024 as another avenue to extract value from less critical assets. We saw a near-record-breaking pace of divestitures by value in 2023. While we don’t expect that pace to continue, we still anticipate divestiture activity higher than a typical year. Completion of significant 2023 divestitures will stretch into 2024, ensuring activity levels stay higher than average.

We will also not be surprised to see announced or contemplated divestitures turn into joint venture opportunities instead, as companies may see value in the scale afforded by combining like-for-like business units that may no longer be core to either company’s operations. Overall, the variety and types of deals we expect to see in 2024 will be far more diverse than what we’ve seen in the market in recent years.

Life sciences corporate divestitures 2018-2023

Slalom contributors: Alex Torgerson, Savina Kalra